This morning, I had my annual managed portfolio review call with Luke Brown, an Investment Management Consultant at Fidelity Investments. I’m especially grateful for their thoughtful insights and actions during this turbulent market.

Fidelity has 3 principles of investing

1. Asset Mix – which is personalized (more about that below)

2. The outside economic / business cycle of the market

3. Maintenance – the constant re-evaluation based on the 2 principles above

They recommend 3 buckets of portfolio assets

1. Cash emergency fund

2. Protected income – social security income and pensions

3. Growth – investments that compound over time

Finally, they consider 3 main inputs for the asset mix of the portfolio

1. Personal risk comfort (on a scale from 1 – 10)

2. Age / time left in market before retirement and withdrawal needs in the retirement

To factor in all of this they use something called a Monte Carlo Analysis. They model how much money someone will have left at the time of their passing based upon the assets they have at the time of retirement, their retirement age, a potential age of their passing (which conservatively I have as 94 years old), the rate of withdrawal depending upon how they want to live in retirement, and three market scenarios – average, below average, and significantly below average.

3. A principle known as Sequence of Return Risk

This principle adjusts the Monte Carlo Analysis based upon different withdrawal rates by year from different accounts (social security, pension, investment accounts, etc.) to find the optimal mix so someone does not outlive their money.

Putting it all together

In the course of an hour talking to Luke, we mapped all of this information and then Luke explained the changes Fidelity recommended for me in real-time.

Two example of how these principles play out for me at this moment in time

1. In a balanced portfolio under average market conditions, foreign stocks are ~21% of an investment portfolio. However, given the current state of the global economy, Fidelity saw that there was additional opportunity in the global markets that match my personal goals, investment level, and risk level so my portfolio has ~25% foreign stocks.

2. A year ago, I was saving to buy an apartment within 5 years. However, over the course of this year that’s changed for me. I now plan to stay in my rent stabilized apartment until 3 years before retirement (when the rent stabilization on my apartment will expire). By that time, I will have saved enough money to buy an apartment. Because that account now has a much longer time horizon, we’ll now invest that account much more aggressively. More time in the market means more compounding and more growth.

Emotions around money

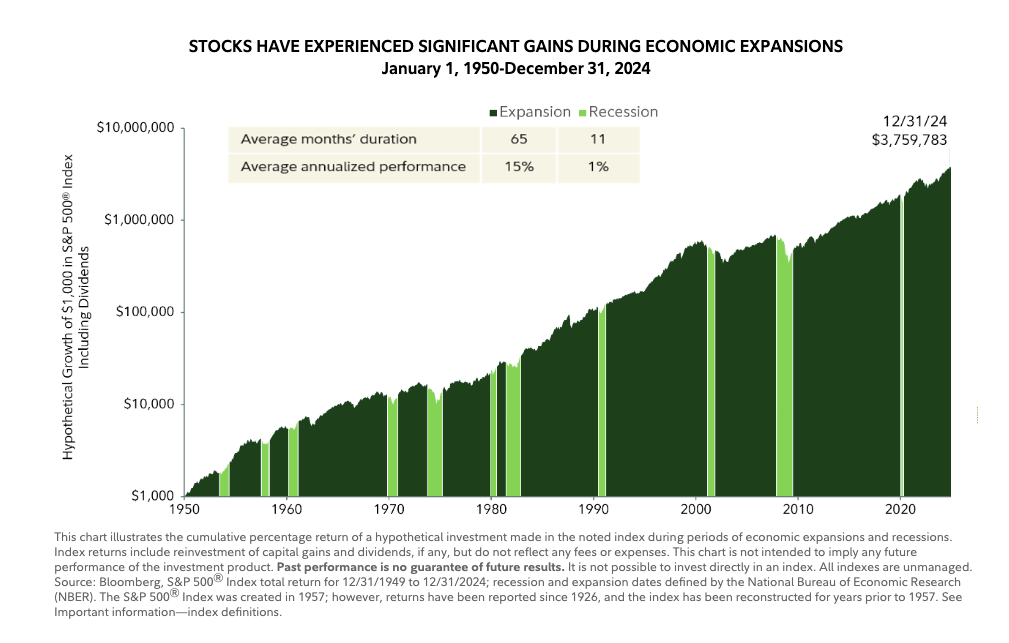

Financial planning is an emotional process. We are talking about the heavy topics of the future and death. Data, when presented as thoughtfully as it is by Fidelity, can bring peace of mind to an emotional discussion. For example, using data from 1950 – 2024, Luke showed me a graph that illustrates recessions (bear markets) last ~11 months. Expansion (bull) markets last ~5 years. So why are we so much more panicked about recessions and less joyful about prosperous cycles? Because loss is painful and dangerous. As humans, we are biologically and neurologically primed to anticipate and protect ourselves from pain and danger. We’re not as primed to be as celebratory and hopeful as we are to worry.

(Since I’m a public historian, here’s a cool piece of secret finance history: The names of the two market types are derived from the animals’ attacking styles: a bull thrusts its horns up (prosperous market), while a bear swipes its paws down (recession). These terms evolved organically in 18th-century London’s Exchange Alley.)

Priming myself for peace

I grew up poor. Because I didn’t have enough, I thought I wasn’t enough. While I have overcome much of that thanks to therapy and a lot of personal work on myself, I remember exactly how I felt as a child. Truthfully, I never thought I’d be able to retire. I assumed I’d have to work until I was dead. Working with Fidelity and people like Luke, I’m hopeful about the future. I printed out that graph about the length of bear and bull markets and taped it up at my desk. This way, whenever these fears about money creep in, which invariably they will, I’ll look at that graph and remember all I have to keep doing is exactly what I’m doing. I do have enough. I am enough.